Today’s Brief

Older Americans are working longer, Washington is tinkering with Social Security, inflation’s “last mile” still bites retirees, portfolios are tilting to safety, and living to 100 is now a planning baseline. We close with Warren Buffett’s end-of-era pivot — what to copy (and what not to). Let’s get practical.

Finance Goals

🧾 Download last 12 months of statements (bank, card, brokerage).

🔔 Add fraud alerts + account notifications (deposit/withdrawal thresholds).

📊 Schedule a 30-min allocation/fee/cash-needs review.

Market Snapshot

📈 S&P 500: 5,2xx

💵 10-yr Treasury: ~4.x%

🛒 CPI YoY: ~3.x% (food & services still sticky)

🏠 30-yr mortgage: ~6–7%

🧓 65+ labor force: multi-decade highs

Indicative only; not advice. Check your platform for live data.

Retirement Redefined: 60–70 Is the New “Flex-Work Decade”

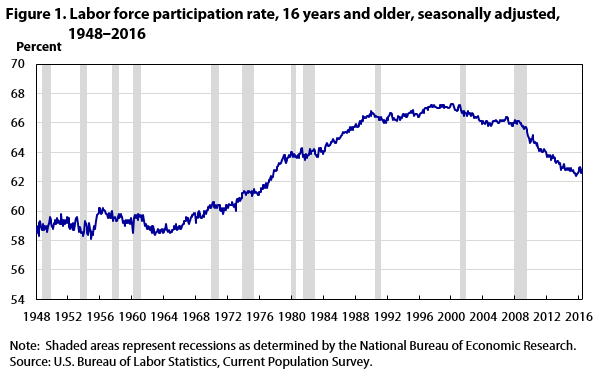

The data: 65+ participation keeps rising

The story isn’t just “people can’t afford to retire.” Many don’t want to — or they want a hybrid version: fewer hours, more control, projects over positions. That shows up in the chart: labor-force participation among Americans 65+ has climbed from historic lows to multi-decade highs. Reasons vary: better health, knowledge work, remote options, and yes, inflation pressure. For employers, it’s a retention story; for workers, it’s a longevity dividend — more years to earn and save, fewer years drawing down.

Older-worker participation is up — flexibility + healthspan = longer careers.

What to do about it

🗓️ Negotiate a phased retirement or consulting retainer (health coverage + schedule clarity).

💵 Use extra income to pad the cash bucket (1–2 yrs of withdrawals in HY savings/laddered T-bills).

🧮 Re-run your plan with delayed Social Security and updated life expectancy — the math may flip.

Seniorish takeaway: Work you like is an asset class. Treat it like one.

Social Security Reform Watch: What a New Bill Could Change

The headline

Lawmakers are floating the most significant tweaks in years: possible changes to the benefit formula, wage-tax cap, and how COLA is calculated. Translation: higher earners may pay more; lower earners could see relatively larger benefits; and an inflation measure that fits retirees better could enter the conversation. None of this is final — but the signal is bipartisan urgency as the trust fund timeline tightens.

What matters to you

⏱️ Claiming age: delaying benefits still boosts monthly income for life; reform won’t change that arithmetic.

👫 Spousal/Survivor benefits: coordinate — the higher earner’s delay often insures the survivor.

🧾 Tax planning: watch the Social Security taxability threshold; consider Roth conversions to reduce future taxation.

Seniorish takeaway: Don’t guess. Pull your mySocialSecurity record, then model scenarios.

Born Today — November 14

🎵 Claude Monet (1840) — patience pays (in art and compounding).

🎭 Butch Cassidy (1866) — not a retirement plan we recommend.

🎤 Josh Duhamel (1972) — longevity is versatility.

Inflation Isn’t Over — It Just Moved Where It Hurts Retirees

The pattern

Headline CPI cooled. But the retiree basket still stings: food-at-home, services (haircuts, insurance, caregiving), and parts of medical services remain sticky. That’s why older households “feel” inflation long after pundits declare victory — our spending skews toward precisely those categories. The fix isn’t denial; it’s design: match rising costs with reliable income and a realistic budget.

Headline inflation down, but services/food haven’t fallen as fast — retirees notice.

Playbook

🔐 Build a bond/T-bill ladder for 1–5 years of withdrawals; keep equity risk for years 6+.

🧾 Audit subscriptions & insurance annually; shop Medicare plans during open windows.

🛒 Buy staples with a list + bulk where sensible; automate price tracking.

Seniorish takeaway: Inflation is now a category problem. Aim precision, not panic.

Stock-Market Seniors: The Quiet Rotation to Safety

What the flows say

Surveys and fund flows point to a gentle drift: 65+ households trimming equities, adding high-yield cash and bonds. That’s not fear — it’s fit. With T-bills and IG bonds paying real income again, you can fund near-term spending without selling stocks into dips. The question isn’t “stocks or not,” it’s “how much sequence-of-returns risk can I stand?”

Older investors are rediscovering the comfort of income — and sleeping better.

Tune-up checklist

🪜 3-bucket system: Cash (1–2 yrs) • Bonds (3–7 yrs) • Stocks (7+ yrs).

🧭 Rebalance bands (e.g., ±5%) prevent emotion-driven trades.

💸 Hold a year of RMDs in cash to avoid forced selling.

Seniorish takeaway: Income calms nerves. Structure beats vibes.

On This Day — November 14

📻 1922: First regular BBC radio broadcast — new channels, new chances.

🛰️ 1969: Apollo 12 launched — precision, not luck.

💽 2006: Google acquires YouTube — platforms change; storytelling stays.

Longevity Risk Looms Large: Plan Like You’ll See 100

The new baseline

More of us will live into our 90s — and beyond. That’s wonderful, and it breaks old withdrawal math. A 65-year-old couple has a meaningful chance one partner reaches 95–100. Markets can cooperate — or not — during those decades. The antidote is boring and effective: layer income sources, delay Social Security where it pays, and size stocks to growth horizons, not feelings.

Longevity isn’t an outlier anymore. Design income that outlives you.

Design your 30-year paycheck

🧱 Floor: Social Security + pensions + SPIA/DIA (if appropriate).

📈 Growth: diversified equities for years 10+; don’t starve future you.

🧮 Rate: test 3.5–4.0% withdrawals through bad decades, not just good ones.

Seniorish takeaway: Hope for 85, plan for 100. Future-you says thanks.

Warren Buffett’s End-of-Era Pivot: Reading the Signals

The news

Warren Buffett’s stepping aside as Berkshire’s CEO at year-end 2025 with Greg Abel taking the helm — a formal handoff long telegraphed, now imminent. Investors are dissecting Buffett’s late-career moves (shrinking some bank bets, doubling down on cash, patient opportunism in energy/industrials) for clues about the next cycle. One non-market lesson: Berkshire also warned of AI deepfakes impersonating Buffett — the scammer’s playbook keeps updating.

Buffett’s last chapter: patience, cash, and circle-of-competence — not bad lessons for the rest of us.

What to copy (and what not to)

- 🧠 Copy: simplicity, cash optionality, and only buying what you understand.

- 🚫 Don’t copy: single-stock concentration unless you are an analyst team.

- 🛡️ Security: treat unsolicited “Buffett tips” as scams; enable 2FA and call back independently.

Seniorish takeaway: The edge isn’t cleverness — it’s discipline.

Linky Links

🧮 SSA account & statement: mySocialSecurity

🧰 Fraud hygiene: IdentityTheft.gov • Have I Been Pwned

💵 Cash ladder helper: TreasuryDirect

🏠 Aging-in-place gear: grab bars • night lights • document scanner

If something here saved you money (or worry), your future self is already grateful.

From Your Seniorish Team 💵

We’re not pros — just curious, well-read friends. Nothing here is investment, legal, or tax advice; talk to a trusted pro before acting.